It is the decision of the management of the organization to follow whichever system suits their needs best. Concerning freedom of systems in managerial vs financial accounting, managerial accounting has few restrictions as to the methods followed. Unlike managerial accounting–which follows internally created rules and processes–financial accounting activities and processes must follow the Generally Accepted Accounting Principles (GAAP).

For every business owner, understanding the roles of both managerial and financial accounting is essential. These two branches of accounting serve different purposes but together offer a complete view of your business’s financial health. When combined, these two approaches give you a balanced perspective and help you understand where your business stands today and where it’s headed. This branch of accounting focuses on recording, summarizing, and reporting financial transactions over a set period.

Internal Reports vs. External Reports

Financial accounting reports must be compliant with the guidelines of IFRS as well as GAAP (Generally Accepted Accounting Principles). Financial accounting reports are most often prepared for submission to government agencies, financial institutions, investors, and the public. It is essential that they adhere to common standards and prescribed guidelines and provide precise information calculated as specified. A financial accountant focuses on the company’s overall finances and whether it is generating a profit. There is no connection or interest in the internal systems of the organization or the day-to-day nitty-gritty. They strive to improve the internal numbers such as efficiency, productivity, etc., and identify and remove bottlenecks to productivity and profitability.

Each serves different purposes, audiences, and offers distinct advantages, depending on your needs. If you want an overview of an entire business or organization, you will need to study the financial accounting reports. The financial accounting reports are of more interest to people outside of the organization. Some of the internal reports would be about inventory, purchase, profits for each individual product, and reports that are aggregated by product, customer, or geography. It is only when some aspect of the business is to be studied in depth that the same person would study both managerial vs financial accounting reports. While both roles require an understanding of accounting principles and financial reports, managerial accountants focus more on business analysis and strategic decision-making.

Reporting Focus and Frequency

- This should not be compromised because it makes the financial situation more prone to non-compliance and legal challenges, which can damage a startup’s reputation.

- The financial statements are typically generated quarterly and annually, although some entities also require monthly statements.

- Each serves different purposes, audiences, and offers distinct advantages, depending on your needs.

- The biggest practical difference between financial accounting and managerial accounting relates to their legal status.

- External parties will then use this information to make decisions that will affect the relevant organization.

- This means your business will always meet accounting standards on how financial transactions are supposed to be recorded and reported to external authorities.

In contrast, managerial accounting is aimed at internal stakeholders—managers and executives within the company. This type of accounting focuses on providing detailed, relevant information that helps in decision-making, strategic planning, and operational control. The reports generated in managerial accounting are often more specific and customized to meet the needs of managers who want to optimize performance and efficiency across departments.

Reporting Focus

These documents are meticulously crafted to reflect the company’s financial performance over a specific period, providing insights into its profitability, liquidity, and solvency. The objective is to offer a clear, standardized view of the financial state of the company, ensuring that external entities have a reliable basis for evaluating the company’s economic activities. Choosing between financial accounting and managerial accounting depends on your career goals or business needs. If you’re interested in working with external stakeholders and are drawn to roles that involve compliance and reporting for investors, then financial accounting might be the right path for you.

This data-driven approach helps a business focus its resources on the most profitable areas and decide whether to invest or cut back. In this way, managerial accounting helps ensure that a business stays competitive and financially sound. Managerial accounting can also be seen as a controlling framework because it monitors and regulates an organization’s activities to ensure it meets its objectives. It includes everything from setting performance standards to comparing them against actual outcomes so that any variances can be timely verified. This is necessary to ensure the management knows the reason for the decline in performance (if and when that’s the case) and what corrective measures they need to take.

Is Managerial Accounting Harder than Financial Accounting?

You may also need to monitor bank statements, investments, and more, requiring similar steps to preparing financial statements for a business. Financial accounting has some internal uses as well, but its focus is on informing those outside of a company. The final accounts or financial statements produced through financial accounting are designed to disclose the firm’s business performance and financial health. Managerial accounting is not bound by external reporting standards, giving organizations the flexibility to design reports that suit their unique operational needs. This customized approach allows for timely and relevant information that supports day-to-day management and long-term planning. While financial accounting looks at the past by analyzing financial information, managerial accounting looks at the future by examining financial information to make forecasts.

They are generated using accepted principles that are enforced through a vast set of rules and guidelines, also known as GAAP. The information generated by the management accountants is intended for internal use by the company’s divisions, departments, or both. Managerial accounting is much more flexible, so the design of the managerial accounting system is difficult to standardize, and standardization is unnecessary. Different companies (even different managers within the same company) require different information. The most important issue is whether the reporting is useful for the planning, controlling, and evaluation purposes. The general purpose of financial statement reporting is to provide information about the results of operations, financial position, and cash flows of an organization.

- Managerial accounting is only concerned with the value these items have on a company’s productivity.

- Financial accountants must conform to certain standards to maintain the company’s publicly traded status.

- Financial accounting must follow certain standards in accordance with GAAP, which is a requirement for businesses based in the U.S. to maintain their publicly traded statuses.

- Financial accounting has a broader focus, providing data and information to external parties.

- Meanwhile, managerial accounting looks at past performance but also creates business forecasts.

- However, without financial data, solving these problems would be much more time-consuming and probably ineffective.

These reports follow strict standards based on Generally Accepted Accounting Principles (GAAP) and are designed for external use by stakeholders such as investors, creditors, and regulatory bodies. In the U.S., the financial accounting reports of a company are governed by the Generally Accepted Accounting Principles (GAAP) as adopted by the U.S. Conforming to these rules allows lenders and investors to directly compare companies based on their financial statements. Managerial accounting information is aimed at helping managers make well-informed business decisions on the direction of the company. Financial accounting reports a company’s performance for a specific period of time and does it in the most straightforward way possible.

Scaling Operations

If you only ever looked at one side of that coin, your knowledge of the company would be incomplete. Ideally, your business needs both sides — managerial accounting and financial accounting — to be successful. Managerial accounting is interested in the systems of your business and reducing problems and streamlining operations therein.

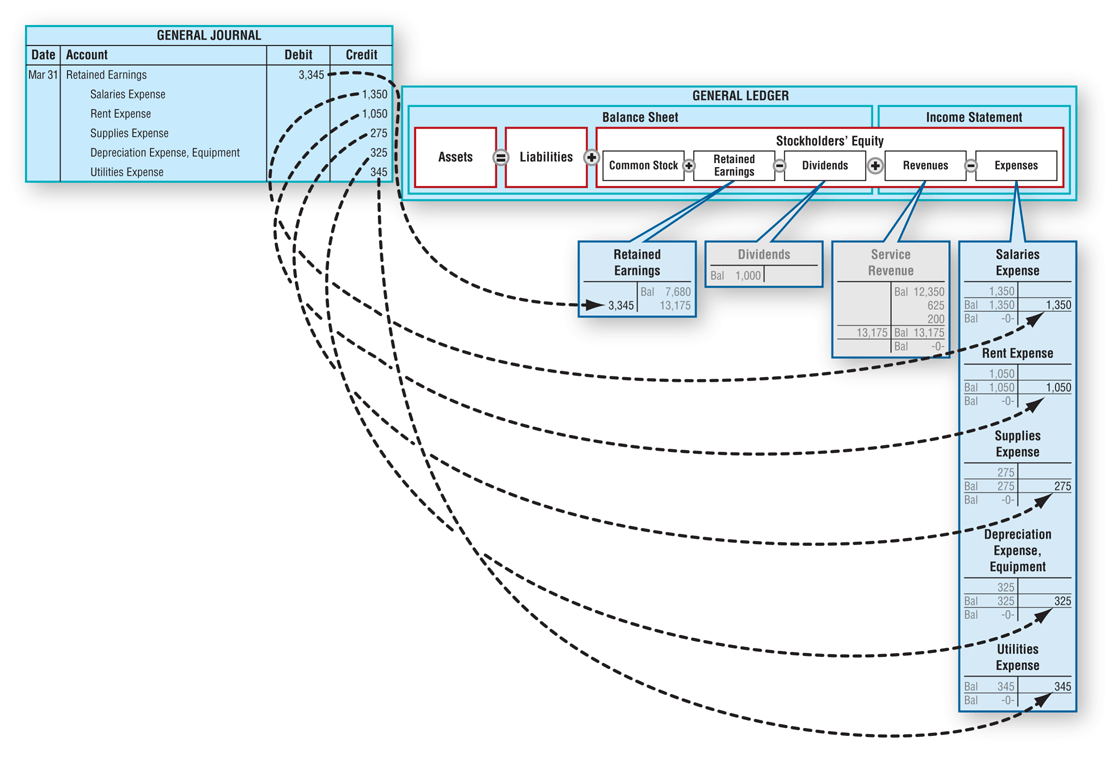

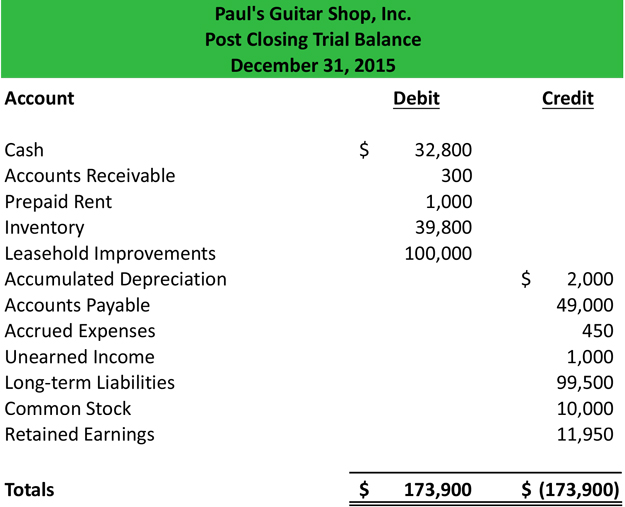

Its primary purpose is to provide an accurate and standardized overview of a business’s financial performance and position over a specific period. This information is compiled into predetermined overhead rate financial statements, such as the balance sheet, income statement, and cash flow statement. The reports generated by the different systems of accounting are also based on their focus. Financial accountants create financial reports and statements to be shared with the investors, owners, stakeholders, the public, financial institutions, and government institutions.

They work internally to meet the needs of clients, customers, or other outside entities that do not work directly with the company but can affect or be affected by the business or projects. Typical responsibilities in this type of accounting can include gathering and maintaining historical data to create reports such what are the invoice processing steps as income statements, cash flow statements and balance sheets. These internal users may include management at all levels in all departments, owners, and other employees.

Still, they need certifications, such as getting a CPA (certified public accountant) license to expand job opportunities. And those wanting to pursue managerial accounting should get a CMA (certified management accountant) credential. Two significant accounting branches are Financial Accounting and Managerial Accounting.

Managerial accounting often combines financial data with operational and even non-financial information, giving decision-makers a more complete understanding of where improvements can be made. Managerial accounting isn’t controlled by reporting deadlines, so your managerial accounting team may produce reports at any time (e.g., weekly, monthly, or whenever requested). Financial accounting, on the other hand, is strictly regulated by a vast number of basic, intermediate, and advanced accounting standards. The fact that the U.S. tax code contains more than 73,000 pages is indication enough of the high standards set on financial accounting.

When managerial accounting is made for internal consumption there is no set of standards to compile that information. Whether it how to report taxes of a municipal bond bought at a premium is financial accounting or managerial accounting – a business needs both to survive and grow. Financial accounting caters to measuring the overall performance, while managerial accounting gives you insights into making organizational decisions.